Market Watch: A Return to Traditional Brokerage Patterns

With the main spring boat show season now behind us, brokerage activity through May suggests a market that is still moving, although at a more measured pace than the same period last year. Fewer yachts changed hands overall, but total sales value remained slightly ahead year-on-year, supported by continued activity in larger motor yacht segments and several significant transactions at the top end of the market.

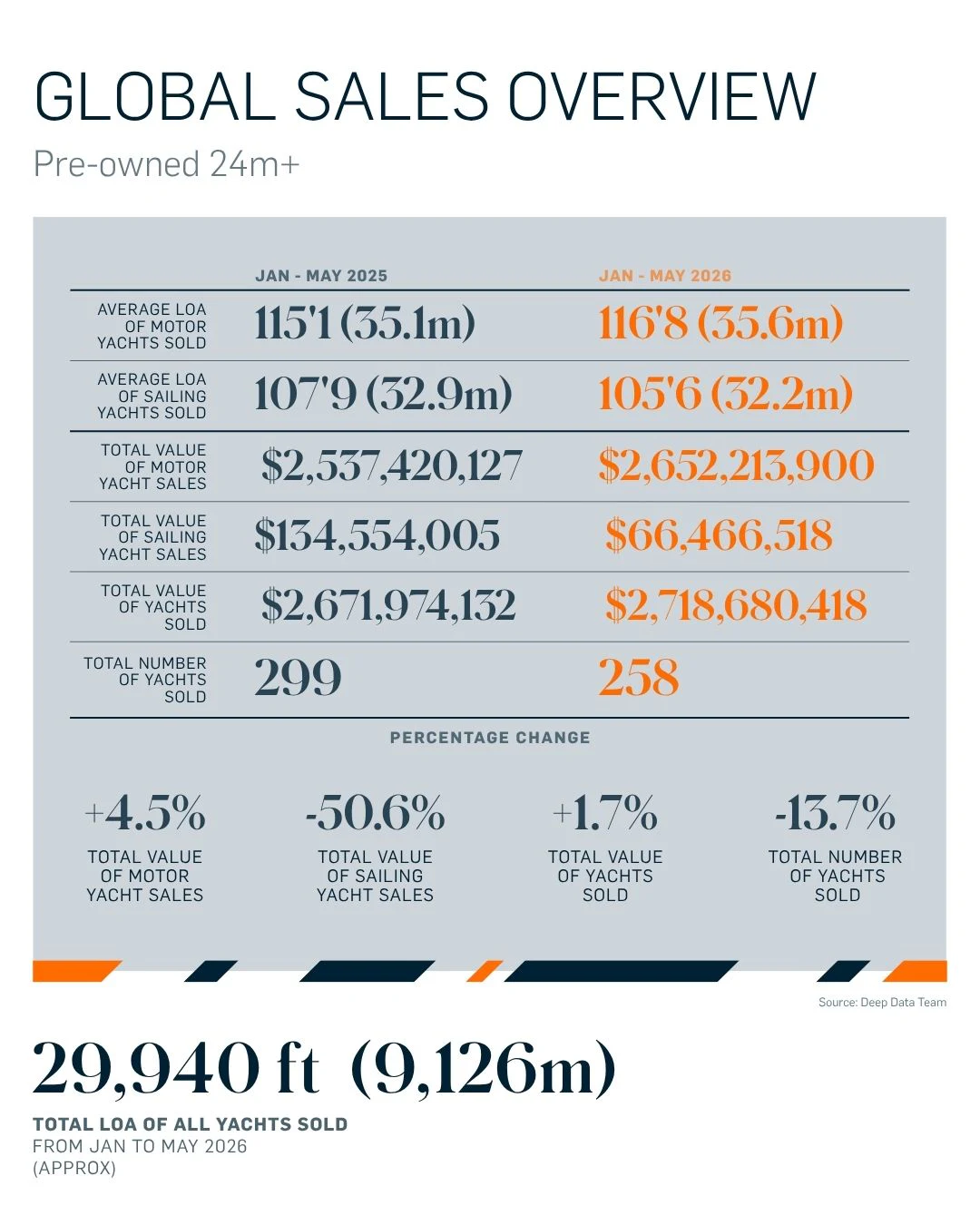

Global Sales Overview

Between January and May 2026, a total of 258 yachts over 79’ (24m) sold globally, down 13.7 percent compared to the same period in 2025. Despite this drop in transaction volume, overall brokerage value increased 1.7 percent year-on-year to approximately $2.72 billion.

This contrast between lower sales numbers and overall value has become one of the clearer trends of the market so far this year. Activity has slowed across the traditional, smaller-sized segment, while larger, higher-value motor yachts have continued to support overall sales figures.

Motor yacht sales value increased 4.5 percent year-on-year to approximately $2.65 billion, despite fewer transactions, while the average length of motor yachts sold remained around the 114’ (35m) mark. Sailing yacht activity, however, has slowed more noticeably, with total sailing yacht sales value falling by more than 50 percent compared to the same period in 2025.

Brokerage Sales by Size Segment

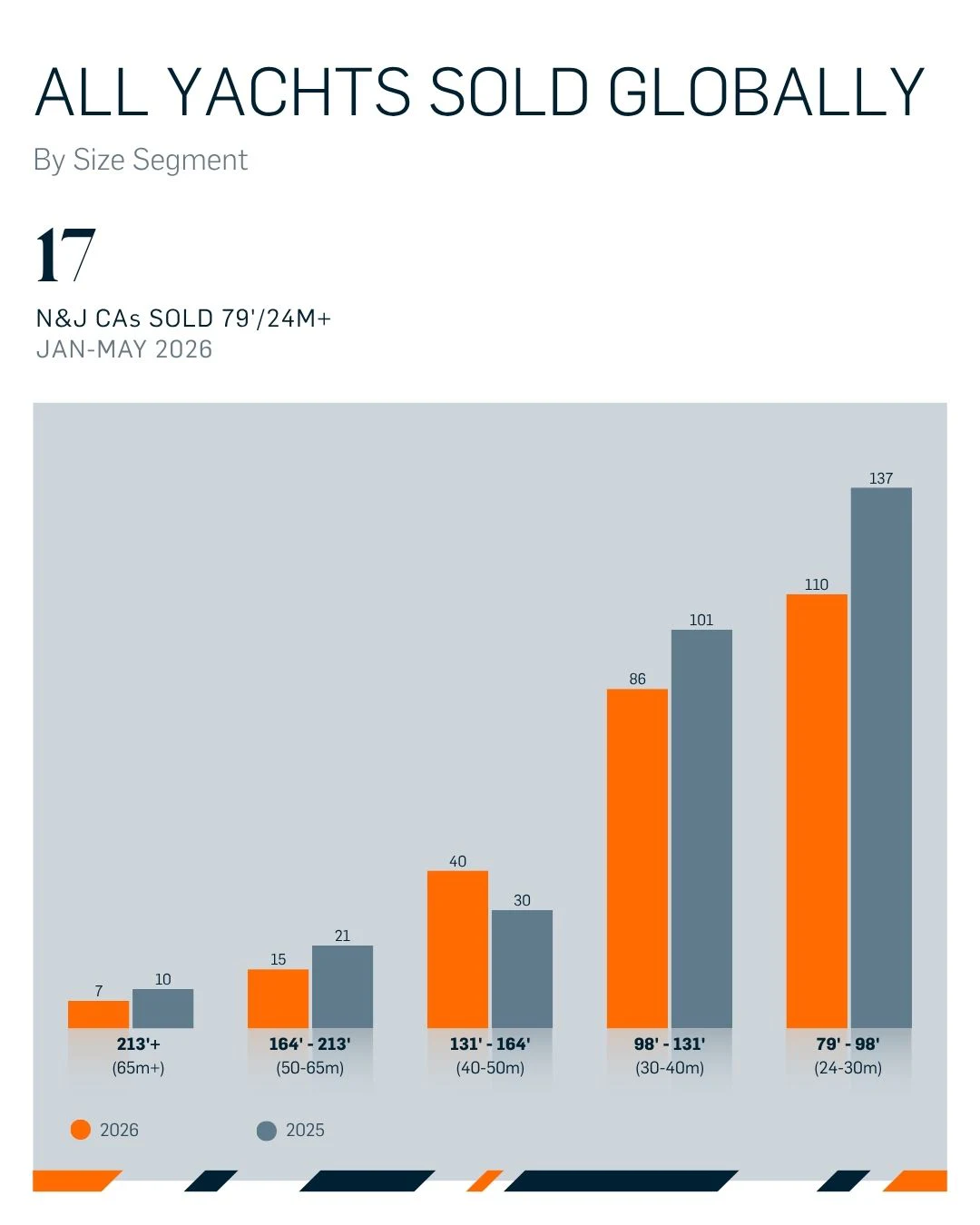

The reduction in overall sales volume has been concentrated primarily within the core brokerage segments. Both the 79’–98’ (24m–30m) and 98’–131’ (30m–40m) segments recorded year-on-year declines and together account for most of the overall drop in transactions.

By contrast, the 131’–164’ (40m–50m) segment was the only category to see year-on-year growth through May, increasing from 30 sales in 2025 to 40 sales in 2026. It continues to be one of the most active areas of the brokerage market, particularly for established pedigree motor yachts.

The 164’+ (50m) categories also held up relatively well compared to the wider market, suggesting demand at the top end remains steadier than within the smaller size brackets. At the very top of the market, a small number of landmark transactions continue to influence overall sales value. The sale of the 404’ (123m) Lürssen-built GOLDEN ODYSSEY remains the largest brokerage sale of the year to date and demonstrates the impact individual ultra-high-value deals can have on the wider market.

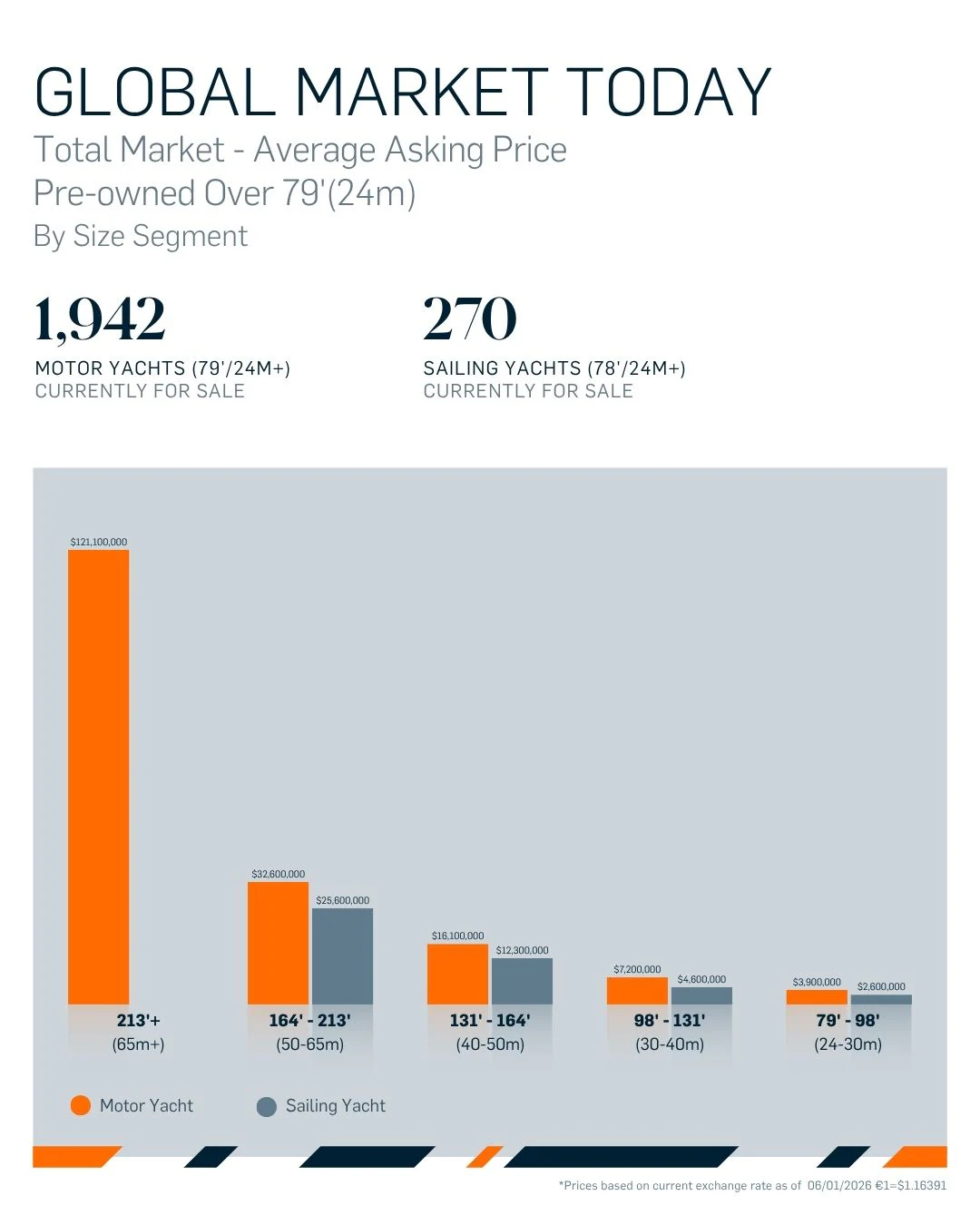

Brokerage Market & Supply

Supply levels remain high, with approximately 1,942 motor yachts and 270 sailing yachts over 79’ (24m) currently listed for sale. Buyers, therefore, continue to have substantial choice across most sectors of the market.

New Central Agency activity has remained broadly consistent year-on-year, with 571 new CA listings entering the market through May compared to 563 during the same period in 2025.

Pricing pressure has become more noticeable, with 4.5 percent more price reductions year-to-date than the same period in 2025. The total value of those reductions increased by more than 11 percent, reaching approximately $808 million.

Taken together, these figures suggest buyers remain active, as long as yachts are well-presented with realistic pricing, while aspirational pricing is meeting greater resistance than during the post-pandemic surge period.

Northrop & Johnson Activity

Northrop & Johnson’s brokerage activity through May reflects these wider market conditions, with continued movement across the core 98’–164’ (30m–50m) range alongside selective larger transactions.

The company completed 17 Central Agency sales over 78’ (24m) year-to-date through May 2026. Recent transactions include the 154’ (46.9m) STAR DIAMOND and the 143’ (43.6m) SHADOWL, reinforcing continued buyer demand for established, pedigree yachts within the mid-to-large size categories.

New listing activity has also remained healthy, with a continued flow of fresh Central Agency appointments entering the market across a range of sizes and price points.

Brokerage Market Outlook

Current conditions suggest a market returning to more traditional brokerage patterns following the unusually accelerated market seen during the immediate post-pandemic period. Buyers remain active, although sales processes are generally taking longer and purchasing decisions appear more focused around value, operational history and long-term ownership costs.

At the same time, activity within the larger motor yacht sectors shows that demand remains present for the right yachts, particularly where pricing, specification and pedigree combine.

Looking ahead to the second half of 2026, inventory levels, pricing and wider macroeconomic confidence are likely to remain the key influences on brokerage activity. While overall transaction numbers may remain below the levels seen in recent peak years, the market continues to perform steadily for quality, well-priced yachts.

As with all market reporting, these observations should be viewed as indicative rather than definitive, with sales data continuing to evolve as additional transactions are reported through the year. Market insights and analysis are powered by data provided by Christina Murphy and Northrop & Johnson’s Deep Data team.

Read Next

Navigator Newsletter Stay informed on all things yachting and luxury lifestyle with the bi-monthly Navigator newsletters.